Article

Understanding the Recent Amendments to the Stamp Act 1949: A Q&A Guide

Article

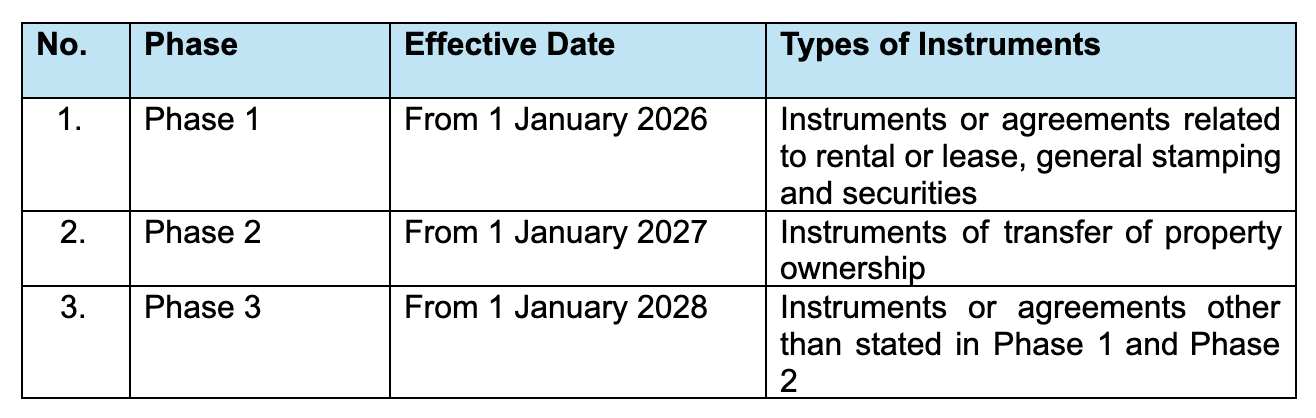

The Measures for the Collection, Administration, and Enforcement of Tax Act 2024, Part IV, introduces several amendments to the Stamp Act 1949, most notably the implementation of the Self-Assessment Stamp Duty System (“Self-Assessment System”) which will come into force on 1 January 2026. As outlined in the Malaysia Budget Speech 2025, the Self-Assessment System will be implemented in phases based on the type of instrument. The schedule of the phased implementation is as follows:

To better understand the practical implications of the recent amendments to the Stamp Act 1949, we have compiled a series of Q&As in a frequently- asked-questions format based our understanding of the current legal framework. These FAQs should be considered within the context of any future guidelines by LHDN on the new provisions to the Stamp Act.

Q: What must I do under the Self-Assessment System?

A: You are required to submit electronically a return together with the duty chargeable instrument. The return must specify the description of the instrument, the amount of duty chargeable and any other particulars as required by LHDN.

(Section 35A)

Q: When do I have to submit the return?

A: Under the current law, the timeline to stamp an instrument is within 30 days from the date of execution if the instrument is executed within Malaysia.

If the instrument is executed outside Malaysia, it must be stamped within 30 days after it has been first received in Malaysia.

(Section 47)

Q: What happens after I submit the return?

A: Upon submission, LHDN is deemed to have made an assessment based on the information in the return. This means the duty amount you submitted is accepted, and the duty is due and payable on the day of assessment.

(Section 36(1)(a), (2))

Q: Is the stamp duty assessment I submit online considered final?

A: No. LHDN may conduct an independent assessment and decide if the correct amount of duty has been declared. If more duty is payable, LHDN will assess and charge the correct amount.

[Section 36(1)(b)]

If LHDN requires more details to properly decide how much duty is payable, they may request for an abstract of the instrument, an affidavit explaining all the facts about the transaction relating to the duty chargeable, including purpose of the transaction, the parties involved and the value of the assets.

[Section 36(2A)]

Q: What happens after I pay the stamp duty?

A: After LHDN determines that the instrument has been fully stamped or the correct duty as assessed by LHDN has been paid, LHDN will certify the instrument by making an endorsement on it. This endorsement will state that the full duty or minimum duty, initial duty, advance duty or additional duty, as the case may be, has been paid. It will also specify the exact amount of duty that was chargeable and paid.

(Section 37)

Q: What are the consequences of not submitting the return?

A: It is an offence if you fail to furnish a return with the instrument without reasonable excuse. If convicted in court, you could be fined up to RM10,000.

[Section 72C(1)]

If no prosecution is brought, LHDN can impose a fine of at least RM200 and not exceeding RM2000 for failing to submit the return.

[Section 72C(3)]

Q: What are the consequences for omitting or understating the duty payable or providing incorrect information on the chargeable duty?

A: You may be guilty of an offence if you submit an incorrect return unless it is proven that the incorrect return was made in good faith. If convicted in court, you could be fined between RM1,000 and RM10,000 and special penalty equivalent to the underpaid duty. For example, if you underpaid RM20,000 in duty, you would have to pay that amount as penalty in addition to the fine imposed.

[Section 72D(1)]

Even if no prosecution is brought, LHDN can impose a penalty equivalent to the underpaid duty.

[Section 72D(2)]

Q: Do I have to retain the instrument and other relevant documents after making payment?

A: Yes, this requirement takes effect from 1 January 2026.

(Section 35B)

Q: How long do I need to keep the instrument and other relevant documents?

A: You are required to keep the instrument and all relevant documents for 7 years from the date of duty payment.

(Section 35B)

Q: What happens if I do not retain the records for 7 years?

A: LHDN may issue a written notice requiring any person to attend personally to produce any instrument, book, account, record or other document or deliver the same, within the time specified in the notice.

[Section 3A(1)(a) and (b)].

If LHDN initiates an audit ****and you ****cannot produce the records without reasonable excuse, on conviction, you could be punishable with a fine of up to RM10,000 (Section 72B)

Therefore, it is best practice to always retain copies of all relevant documents for at least 7 years to avoid complications in the event you are selected for an audit.

Q: Can LHDN enter and search my premises?

A: Yes, LHDN has the power to enter all lands, buildings and places to conduct searches and inspection.

[Section 3A(2)]

Q: What can LHDN search and inspect?

A: LHDN’s search and inspection powers under the amended Section 3A extend beyond documents to include objects and things. This would include powers to search items like computers, mobile phones and hard drives, that may contain relevant information.

[Section 3A(2A)(a)]

Q: Can LHDN seize items from my premises?

A: The Stamp Act does not explicitly provide LHDN the power to seize items. However, LHDN may extract and make copies of the documents or items during the inspection. For example, LHDN can duplicate digital data from electronic devices.

[Section 3A(2A)(b)]

Q: What must I do if LHDN visits my premises for search and inspection?

A: You should render cooperation in the search and inspection by:-

- providing access to storage rooms, safes, or digital databases and other places where necessary records or instruments are kept; and

- provide information or explanations if requested.

You must also offer basic facilities to enable LHDN to conduct the inspection effectively such as a workspace, lighting, and basic amenities like access to restrooms if the search and inspection is lengthy.

Section 3A(2B)

Q: Can LHDN request for translation of documents not in Malay language?

A: In Peninsular Malaysia, if LHDN needs to check documents not in the Malay language to determine how much stamp duty should be paid, LHDN may issue a written notice requiring a translation of the document into the Malay language.

In East Malaysia, LHDN may request for a translation where the documents are neither in the Malay language nor in English.

[Section 3A(3A)]

Q: If I receive the written notice requiring translation of documents, when do I need to submit the translation to LHDN?

A: The written notice will specify a timeframe for compliance, which must be at least 30 days from the date the notice is served.

[Section 3A(3A)]

Contact

_resize.jpg)

Chong Yeong Yoong

Related Publications

Chambers & Partners Asia-Pacific 2024 Guide - S. Sivaneindiren

The Law on Land Acquisition

Pang Kong Leng